|

|

|

|

|

Desperate to Boost Oil Production, Venezuela Moves to Devalue Currency

By Nick Cunningham

On December 16, 2013, Venezuelan President Nicolas Maduro outlined plans to use a weaker exchange rate in order to lift the prospects of its ailing oil sector and deal with a worsening economic crisis. Venezuelas foreign exchange reserves have depleted to their lowest levels since 2004. The weaker exchange rate allows the government to earn more Bolivars for every barrel of oil sold, which is priced in dollars on the international market.

The measure appears to apply only to oil transactions. The official exchange rate in Venezuela is 6.3 Bolivars per dollar, while the alternative exchange rate used for oil sales hovers near 12 Bolivars per dollar, according to the Wall Street Journal. Unofficially, exchange rates on the black market often mean people pay as much as 60 Bolivars for every dollar.

Related article: Why are Gas Prices Falling, and How Long will the Trend Last?

The de facto currency devaluation comes as the economy continues to deteriorate. Yields on Venezuelas sovereign debt reached 15% in early December. Standard & Poors and Moodys Investors Service, two credit rating agencies, both downgraded Venezuelas credit rating in mid-December, citing growing radicalization of the economy.

The battered economy has also pushed President Maduro to consider raising gasoline prices. Heavy government subsidies result in Venezuelans paying some of the lowest prices at the pump in the world around 5 cents per gallon. Subsidies are not only expensive for the government, but they also discourage efficiency, and higher domestic consumption eats into potential exports. Slashing subsidies will reduce this enormous fiscal burden, which can cost the government around $12.5 billion per year.

However, Maduro is in a bind because raising gasoline prices and devaluing the currency will only exacerbate inflation, already running at around 54% per year. Stoking inflation will squeeze the Venezuelan people further, already reeling from unemployment and shortages of food.

President Maduro has sought to maintain a grip on all powers of government, following in the footsteps of the late Hugo Chavez. On November 19, the Congress passed, and Maduro signed, a law that grants the President power to rule by decree for the next year. He argues the powers are needed to clean out corruption and reduce the harmful influence of capitalist forces. Buoyed by the populist maneuver, Maduros party won municipal elections on December 8, which has given him enough political capital to pursue risky maneuvers to head off a worsening economic crisis.

Related article: Amid Declining Latin American Output, Colombian Oil is Booming

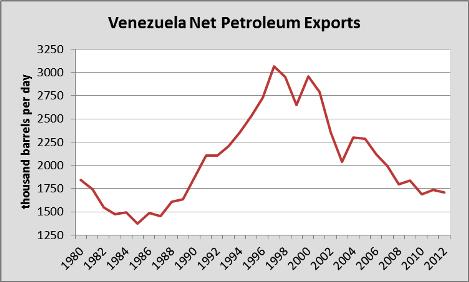

The Maduro government is entirely dependent on its flagging oil industry. Venezuela holds the second largest oil reserves in the world at 211 billion barrels. Oil represents 95% of export earnings and about half of budget revenues. Yet Venezuelas oil exports have declined by nearly half since peaking at 3 million barrels per day in 1997. Natural decline of the nations oil fields is a contributing factor, but the mismanagement of Petróleos de Venezuela (PDVSA), the state-owned oil company, is the greater reason for decline.

Venezuela Net Petroleum Exports

Source: EIA

In late November, Citigroup published a report concluding that Venezuela presents, probably the biggest bull risk to the oil market in 2014 outside of the MENA [Middle East and north Africa] region. Venezuela is struggling to pay its debts, and the government is pillaging PDVSAs coffers as it searches for cash. Without money to invest in its oil fields, even if Venezuela can avoid a more acute crisis, such as debt default or a coup, its oil output will decline over the long-term.

By. Nick Cunningham